Tips on Starting a Syndicate

.png)

Brian Nichols is the co-founder of Angel Squad, a community where you’ll learn how to angel invest and get a chance to invest as little as $1k into Hustle Fund's top performing early-stage startups

When I ask seasoned investors the best way to get good at investing, they all say the same thing: start a syndicate.

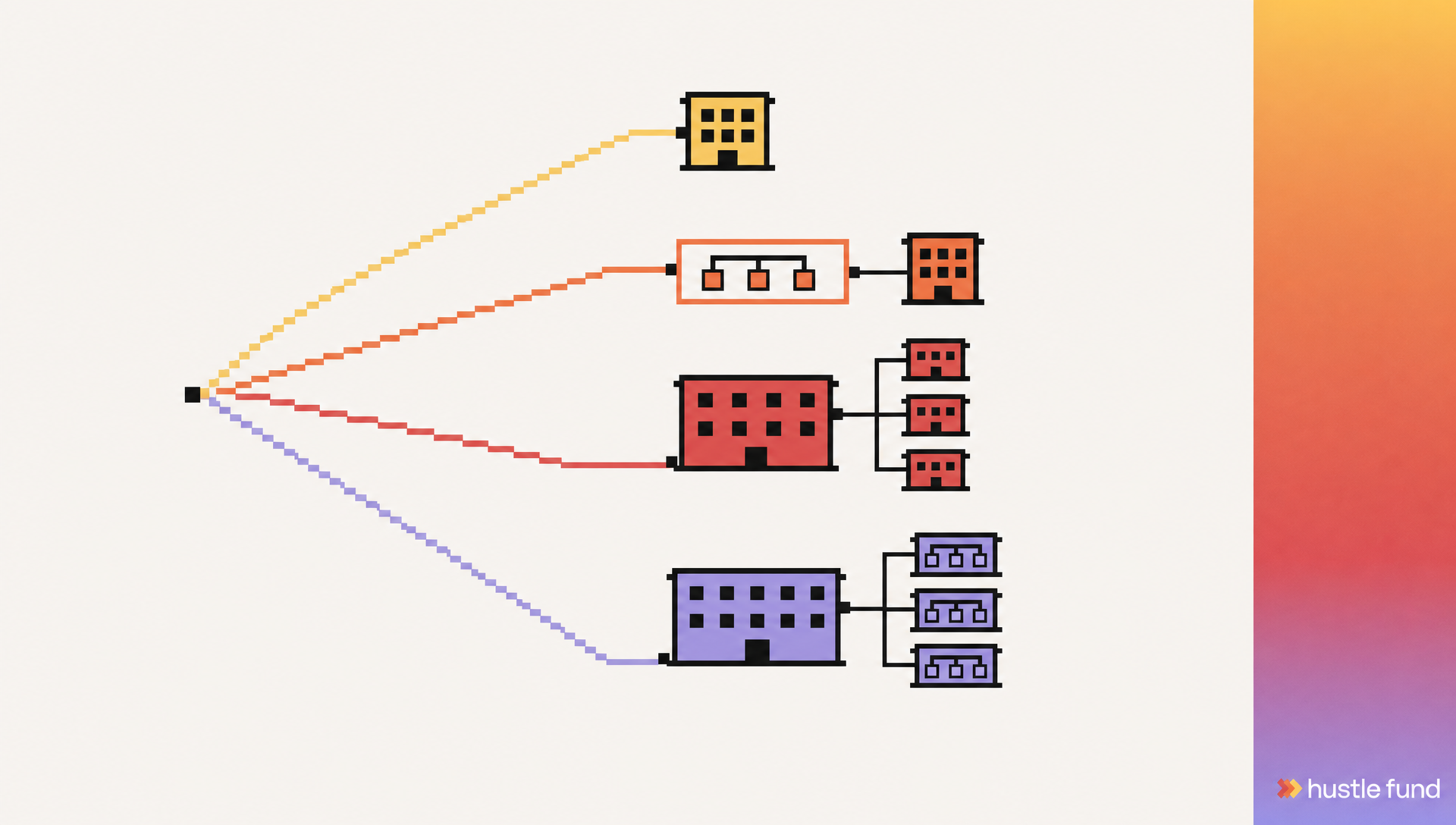

Real quick: a syndicate is a group of investors that pools their money to invest in a deal.

Mechanically, syndicates run through SPVs (special purpose vehicles); we've explained how these work and what investors should know in our SPV guide.

The cool thing about being in a syndicate is that you get the same terms as the lead investor.

But there's no pressure to invest in any deal unless you want to.

As an angel investor, being part of a syndicate is a great way to get access to dealflow without going out and finding the deals yourself.

But being in a syndicate and starting a syndicate are two totally different things.

So I sat down with Brian Nichols, an investor (and my colleague) who runs two successful angel syndicates: the Uplyft Syndicate and Angel Squad.

Between these two syndicates, Brian has helped 70 startups raise a total of $25m in funding from around 2,500 investors.

Here are some of his learnings around starting and running a syndicate.

Getting investors to join

The first thing a syndicate needs is investors. Otherwise you won't be able to fill allocation in your deals.

But with so many syndicates out there, it can be hard to convince someone to join yours.

With Uplyft, Brian's strategy was to convince his former Lyft colleagues that there was no downside to joining.

First, he made a list of people he knew would be value-add advisors.

Then he told them:

"It's totally free to join, and I'll do all the hard work. I'll source the deals, I'll write the deal memos. You'll get a chance to check out startups across different industries. If you like them, you can invest at great terms. If you don't, you skip. And if you're curious about what they're doing, maybe you could mentor them and learn more."

If you're going this route, your investors will likely ask about carry, the percentage of profits the syndicate lead earns. Our beginner's guide to carry breaks down how it actually works.

This approach helped Brian bring on the first investors for the Uplyft Syndicate.

Getting dealflow

Once he lined up his investors, Brian needed dealflow.

He started with friends who were early-stage founders. He asked if they were raising and what the terms were.

Then he asked them this question:

"Would access to a small army of Lyft talent be helpful for you?”

Unsurprisingly, all the founders said yes.

By finding investors for the syndicate that were knowledgable about early-stage startup operations and growth, Brian gave his syndicate an edge.

Founders recognized this wasn't just "dumb money" and were willing to give up allocation.

The more deals the syndicate won, the more investors who wanted to join. The more investors who joined, the more dealflow they got.

And thus the flywheel was born.

Validating the deals

As with any investor, syndicates only want to invest in companies that have strong signalling.

But as someone with a family and a full time job, Brian doesn't have time to review every deal that comes his way.

This is where having a partner is key.

Validation also depends on rigorous due diligence; our breakdown of the different levels of due diligence shows what each stage requires.

When founders approach Uplyft for investment, Brian does an initial pass. Then he typically sends the top contenders to his partner Ann Miura Ko – managing partner at Floodgate – to review before sharing them with the larger community.

This is a win-win-win process.

Brian wins because he doesn't have to shoulder all the work.

Ann wins because she gets to sift through dealflow for her venture fund while helping the syndicate.

And the syndicate wins because they're only seeing deals that have been thoroughly vetted.

Marketing the deals

The best way to continually win dealflow is to have a syndicate that regularly fills (or almost fills) allocation.

It's up to the syndicate lead to make sure that happens. And according to Brian, this is where most of the work is.

In fact, syndicates are often managed by co-leads because marketing the deals takes so much time.

In the case of Uplyft, Brian will send three messages to the syndicate about a deal.

These are not your standard boiler plate memos. Each message is individually crafted to highlight the startups' strongest selling points:

- why this is the right team to solve this problem

- data showing they understand their customers

- evidence they can sell their product

- scope of the market

Many of these signals are the same things investors look for during pitch meetings; we've shared the questions to ask during a pitch meeting that surface this information.

Brian recommends being upfront about the risk factors, but feels strongly that his job is to support the founders he's partnering with.

If he feels like he has to hide something from the syndicate in order to fill the deal, it's not the right deal.

Is it worth it?

Given how much work it is to start and lead a syndicate, I had to ask: is it worth the trouble? Why not just join an existing syndicate and let someone else do all the hard stuff?

For most of us, joining a syndicate is enough.

We'll get access to exciting startups at terms that are probably pretty good.

But for others, having your own syndicate is very much worth the effort.

Here are some reasons this might make sense:

1. You want to start your own fund one day

Starting a fund is a LOT of work. Running a syndicate is like a dress rehearsal... you'll get loads of practice at picking companies and fighting for allocation.

You'll also grow your network with people who could be potential LPs one day.

If that's your goal, understanding the risk and returns across stages of venture capital will help you build a thesis that makes sense to LPs.

2. You want to work for a VC one day

VCs want to hire people with investing experience. Running a syndicate gives you practical experience, access to founders who may want to raise again in the future, and a unique perspective that could benefit a fund.

3. You want to invest in specific verticals

Examples: Climate tech companies. Female-founded companies. Companies started by your college alum.

4. You want to invest in alongside certain people

If you're a product person, you may want to start a syndicate made up of product experts.

This could give you an edge over other syndicates who may not be able to add as much value.

Or maybe you want to invest alongside your colleagues from a previous company... people you were in the trenches with, who know how to build a high-growth startup.

Got more questions about starting a syndicate? Brian gets so many questions about this topic that he put together an FAQ doc. You can read it here.

Onward,

Kera from Hustle Fund

.png)

.png)