How SPVs Work in Angel Investing: A Practical Guide

.png)

Brian Nichols is the co-founder of Angel Squad, a community where you’ll learn how to angel invest and get a chance to invest as little as $1k into Hustle Fund's top performing early-stage startups

You find a startup you like. Problem is, your $5,000 check is too small to matter on its own, and the founder really doesn't want 30 separate names cluttering up the round. That's the exact gap an SPV fills. It lets a pile of small checks show up as one organized investment, so the founder deals with one line on the cap table instead of a crowd.

If you've spent any time around syndicates, you've heard the acronym thrown around like everyone already knows what it means. Most people sort of half know. They can tell you it stands for special purpose vehicle, and then the explanation trails off. So let's walk through the whole thing: what an SPV is, who runs it, how the money and paperwork move from handshake to exit, what it costs, the risks that don't show up in the pitch, and when it's worth doing versus when it just adds drag.

What an SPV Is (And Why Angels Use Them)

An SPV, or special purpose vehicle, is a one-off legal entity created to make a single investment in one company. A syndicate lead pools many small investors into it, so the startup sees one line item instead of dozens of names.

Founders optimize for speed and a clean cap table, not admin pain. A well-run SPV turns scattered interest, friends-and-family money, or a follow-on into one coordinated check with one signer and one channel. It's also how angels exercise pro rata when a company raises again, without every backer scrambling on their own.

Small checks punch above their weight, which is part of why angels reach for SPVs. As our very own Hustle Fund GP, Elizabeth Yin, put it: "There have been SO MANY TIMES when a founder has told me the minimum is $25k, and I've just told them, 'Hey, I can't do that, but I can do $1k. I won't be a pain in your side and can open doors.' And you know what, the minimum is dropped." An SPV is just the clean way to pool those checks into one.

SPV vs. Syndicate vs. Fund: What's the Difference?

A syndicate is the people, the SPV is the legal wrapper, and a fund is the long-lived vehicle that invests across multiple deals. That distinction matters because investors say "syndicate" when they really mean the special purpose vehicle that actually signs documents and wires money.

Founders care because a pooled investment through an SPV simplifies cap table management and cuts coordination overhead. One organized SPV beats 40 separate angels asking for side letters, updates, and signatures.

Who This Guide Is For

This guide is for new angels writing roughly $1,000 to $25,000 checks who want into startup rounds without becoming a burden on founders. It's also for lead angels who want to bring others along without creating 40 separate names on one startup's records.

It's especially useful if you're weighing an SPV fund, a traditional angel network, and a community-based model like Angel Squad against each other.

Many newer investors want education, not just deal links. A community that pairs real deal access with content on how to actually evaluate companies tends to be the bridge between being curious about angel investing and doing it with some discipline.

.jpeg)

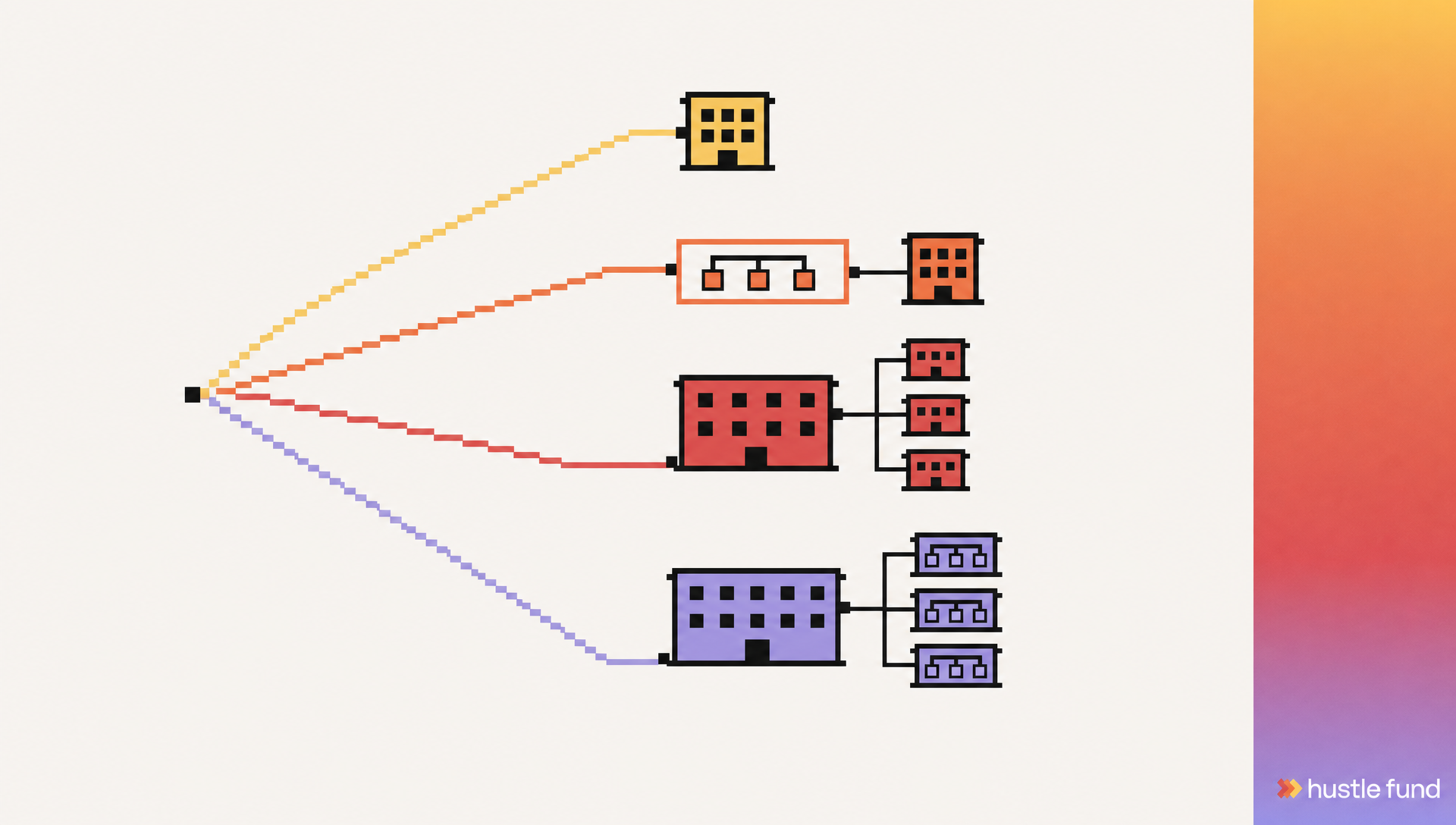

The Players in an Angel SPV (And What Each One Does)

Every angel SPV has four parts: a manager who runs it, the investors putting in capital, the startup receiving the money, and the service providers keeping the machine from melting down. One party runs the vehicle, and everyone else relies on that party to execute.

Investors are usually limited partners or members, and the manager acts like a general partner or managing member. An LLC wrapper keeps the investment separate from investors' personal affairs, which is part of why angel and venture deals use it. The startup's side is simple, one aggregated check and one signatory. Service providers (platforms, counsel, fund admins, banks, tax preparers) exist to cut error risk, which is what turns a clean SPV into an administrative mess.

What the SPV Manager Is Responsible For

The manager handles KYC, AML, investor onboarding, document execution, banking, and distributions. On platforms like AngelList, much of that workflow is standardized, but standardization doesn't remove responsibility. Someone still has to chase signatures, resolve late wires, and make judgment calls when edge cases show up.

The manager also tracks ownership, shares updates, handles follow-on rights, and coordinates with company counsel after closing. A competent manager isn't just a deal scout. They're the operating system for the vehicle.

What LPs Should Expect (And Ask Up Front)

Ask about the fee stack before wiring money: management fee, administration fee, setup costs, and carry. If the answers are vague, assume the economics get worse after the fact, not better.

Also ask whether the entity is a bankruptcy-remote SPV, how cash is held before close, and what reporting system is used, whether that's Carta or something else. Operational sloppiness can damage returns even when the startup itself performs well.

How an SPV Actually Works: Step-by-Step From Deal to Exit

The lifecycle is straightforward: a lead finds a deal, forms the SPV, collects subscriptions, closes the investment, holds the position for years, and distributes proceeds after a liquidity event. Founders like it because the company gets one investor record on the cap table even if 50 people are economically behind it.

Two timelines matter more than the rest. The fundraising window is short and operational. The liquidity window is long and uncertain. That gap is the whole game, and patience plus process shape the outcome more than the pitch does. The mechanics also get a lot less abstract once you've watched a few deals run end to end, which is how you learn what's normal versus what's sloppy.

Step 1: Deal Sourcing and Terms (What Gets Negotiated)

The lead sources the company and negotiates the instrument, often a SAFE, a convertible note, or preferred equity. Understand the basics: valuation cap, discount, MFN clauses, and pro rata rights drive future ownership more than the headline story does.

A convertible note adds debt-like features, while a SAFE is usually simpler and common in early rounds. The instrument choice affects timing, dilution, and downside protection, so "simple" documents can still carry meaningful economic differences.

Step 2: SPV Setup and Paperwork

Once the deal is real, the SPV entity gets formed, often as an LLC or LP, and its operating or partnership agreement defines manager powers and investor rights. Investors then sign subscription documents, make representations about accreditation, and complete identity checks.

This stage feels boring, but paperwork quality predicts operational quality. If the documents are inconsistent or the timeline is fuzzy, expect the same friction later when tax forms or distributions are due.

Step 3: Capital Calls, Banking, and Closing Mechanics

After subscriptions are accepted, investors send money through a capital call, usually by wire or ACH. Good operators use segregated accounts and escrow where appropriate, so investor cash isn't casually mixed with unrelated operating funds.

A first close means some investors are in and the SPV can proceed. A final close means the fundraising window is done. That distinction matters because late investors may have different deadlines, and founders care deeply about whether the money is truly committed.

Step 4: Post-Close Operations (The Boring Stuff That Matters)

After closing, the SPV stores documents, tracks the startup cap table position, and sends updates to investors. This is where operational discipline quietly compounds, because missing records today become expensive confusion years later.

The manager may also need to handle follow-on rounds, information rights, or the occasional secondary sale. Most SPVs are simple only if the manager stays organized.

Step 5: Exit and Distributions

If the company is acquired, runs a tender offer, or goes public, the SPV receives proceeds and distributes them according to its waterfall: return of capital first, then carry on profits, then the rest to investors by ownership. (For more on that moment, here's what actually happens during a liquidity event.)

Liquidity can take many years, and partial liquidity is possible but never guaranteed. The biggest mental mistake in angel investing is treating an SPV like a liquid brokerage account when it's really a long-duration private asset.

SPV Structures You'll See: LLC vs. LP vs. "Fund SPV"

Most angel SPVs use an LLC or an LP because both can support a clean cap table and centralized management. The choice affects taxes, admin burden, investor familiarity, and how formal the vehicle feels to founders and co-investors.

Some SPVs are designed to be bankruptcy-remote so liabilities stay ring-fenced from the manager's or platform's other activities. That's less marketing language than operational protection when cash, contracts, and claims need clear boundaries.

SPV LLC

The LLC is common for an angel syndicate because it's flexible and relatively intuitive. A strong operating agreement defines voting, transfers, fees, and distributions clearly, but flexibility only helps if someone actually drafts and administers it well.

Many LLC SPVs are pass-through entities and issue K-1s. That simplicity is real, but it still requires competent bookkeeping and investor reporting.

SPV LP (Limited Partnership)

A limited partnership looks more like a traditional fund, with a GP managing and LPs investing. It can feel more institutional for larger checks or repeat leads who want a familiar venture format.

The tradeoff is that LP structures can feel heavier to administer for small angel deals. If the round is tiny, sophistication on paper becomes unnecessary drag in practice.

SPV Company / Corporate SPV

A corporate SPV is less common in angel deals but shows up for specific legal or tax reasons. Depending on jurisdiction, it can introduce more complexity and possible double-tax issues, which is why most small angel deals skip it unless there's a clear reason.

Economics: Fees, Carry, Minimum Checks, and What You Really Pay

SPV economics include setup costs, admin costs, possible annual expenses, and carried interest to the manager. Investors fixate on access and forget that net returns, not gross outcomes, decide whether a small check actually worked.

The minimum check is a big draw: pooling smaller commitments lets you participate below what you could hit alone while still showing the startup a meaningful total. Just keep platform fees, manager carry, and pass-through expenses separate in your head, since they hit at different times and pass-through tax treatment doesn't make them disappear.

Carry Explained Without the Headache

Carry is a percentage of profits paid to the manager after investors get their principal back, subject to the deal terms. It aligns incentives because the manager shares in the upside, but in a small SPV, fees plus carry can meaningfully compress returns.

A Simple Back-of-the-Napkin Example

Say you commit $10,000 to an SPV investing in an early-stage startup, and the vehicle charges a small setup fee plus 20 percent carry on profits. If that investment later returns $50,000 gross, your net may land closer to the low $40,000s after fees, carry, taxes, and dilution.

That's still a strong outcome, but the gap between gross and net is the lesson. Firms like 500 Startups helped normalize venture-style portfolio thinking, and that matters because one winner can carry the returns while most bets return little or nothing.

Taxes and Compliance: What Investors Should Know (Without Legalese)

Most SPVs are pass-through entities, so taxable items flow to investors rather than getting taxed at the entity level. In practice that means a Schedule K-1 that usually arrives later than you'd like.

Compliance isn't optional. KYC, AML, accreditation checks, and securities exemptions exist because private offerings are regulated, and the rules feel tedious right before they prove useful. State and federal filing requirements vary, and international investors face extra friction from withholding and treaty paperwork.

Do SPVs Pay Taxes?

Usually the SPV itself doesn't pay income tax if it's structured as a pass-through, but it depends on the entity type and jurisdiction. Assume the tax burden flows through to you unless the documents say otherwise.

K-1 timing is its own operational risk, since delays can mess with your personal filing calendar. A manager who can't explain the tax process clearly is signaling future friction.

Common Forms and Checks You'll See

Expect forms like the W-9 or W-8BEN, accreditation checks, and subscription agreement representations. These satisfy securities compliance and anti-money-laundering rules. They aren't there to make your life weird for sport.

When to Use an SPV (And When Not To)

An SPV works well when founders want a clean cap table, investors want access with smaller checks, and the lead can close fast without drama. It also fits co-invest rights and pro rata follow-ons, where pooling reduces coordination friction.

It's a bad fit when the deal is so small that fees eat the upside, the lead's incentives are unclear, or diligence is rushed. And one SPV is not diversification. One SPV means one company and one outcome.

Founder-Friendly SPVs: What Founders Typically Want

Founders want one line on the cap table, one person coordinating signatures, and no surprise side letters. A founder-friendly SPV is invisible in the best way, because it behaves like one competent investor.

Red Flags Before You Join

Watch for vague fee disclosure, unclear allocation policy, and no closing timeline. Ask how tax documents, distributions, and follow-on rights get handled before you wire anything.

Common Mistakes (That Make SPVs Painful) and How to Avoid Them

The biggest SPV mistakes are operational, not theoretical. Missing signatures, late wires, and messy cap table updates create avoidable friction that damages founder trust and investor confidence.

Two more get people every time: not reading the operating agreement (transfer restrictions, voting thresholds, and manager powers matter most exactly when something goes wrong), and assuming liquidity that doesn't exist. An SPV doesn't make a startup easier to exit. It just organizes ownership.

Checklist: What to Review Before You Invest

Review fees, carry, expenses, instrument type, valuation terms, and the closing date. Then review governance: who can make decisions, what investor consent is required, and what happens if the manager disappears or goes unresponsive.

Mistakes Lead Investors Make

Leads get into trouble when they over-promise returns, under-communicate on timing, or treat admin as an afterthought. They also create resentment when they don't set clear allocation rules before an oversubscribed round gets tight.

For a deeper breakdown of carry, fees, and SPVs, see angel investing group terms explained. For context on networks versus going alone, this comparison of angel investor networks vs solo investing is useful.

Real-World Examples: What SPVs Look Like in Practice

Example one: 50 angels each put $1,000 to $10,000 into a pre-seed SAFE through one SPV. Everyone participates at a small check size while the founder keeps one organized investor relationship instead of 50 separate ones.

Example two: earlier backers form a follow-on SPV to maintain pro rata in a breakout company. This is often the cleanest way to preserve exposure when demand is high and individual coordination would slow the round.

Example three: a lead offers a small co-invest SPV to a handful of strategic investors to strengthen future relationships. These work best when the mechanics stay simple, because early-stage outcomes are already high-variance without adding process confusion.

That's one reason Hustle Fund's "hilariously early" framing is useful. At the earliest stages, long timelines and uneven outcomes are normal, so simple mechanics beat fancy structure.

Case Study Template You Can Reuse

Use this template: deal context, instrument, SPV size, fees, timeline, outcome, and lessons learned. Add a final note on what you'd do differently, because honest postmortems teach more than polished victory laps.

If you want to sharpen your pattern recognition, these related reads help: Angel Squad vs a traditional angel network, building an angel network from zero to 100 connections, and following top VCs as a strategy.

FAQ

Do SPVs pay taxes?

Usually no at the entity level if the SPV is a pass-through structure. Taxes generally flow to investors, often through a K-1, though treatment depends on structure and jurisdiction.

What are the disadvantages of an SPV?

The main downsides are fees, paperwork, long illiquidity, and dependence on the manager for administration and communication. If the check size is small, those frictions can take a noticeable bite out of returns.

How could a $5000 investment turn into $1,000,000?

That takes an extreme outlier, roughly a 200x return, with limited dilution and a very large company outcome. It happens in venture, but it's rare and not a sensible base case. The math is about multiples, not ownership. Elizabeth has made the point directly: "If you invested $5k into Uber's seed round and held on to the IPO, you would have made ~$25m. $5k doesn't buy you any ownership. So is that a failed investment? Obviously not." At the earliest stages, your return rides on the multiple, not the percentage you own.

How much do I need to invest to make $100,000 a year?

Angel investing doesn't usually produce steady annual income, because exits are irregular and often take years. Consistent six figures a year would typically require a large, diversified portfolio and multiple liquidity events.

Final Take

An SPV is just a legal wrapper that lets many angels invest in one startup as one coordinated entity. When the manager is competent, the fees are clear, and the deal is worth the concentration risk, it makes small-check angel investing cleaner for everyone. The hard part isn't the acronym. It's judging deal quality, manager quality, and whether the economics still hold up after time, taxes, fees, and dilution do their work.

If you'd rather learn that by doing it next to people who run these vehicles for a living, that's what Angel Squad is built for: a community of 2,500+ angels across 50+ countries who've collectively put $30M+ into 70+ startups, with a no-a-holes policy. Hustle Fund is an early-stage fund, but the deals shared with members run pre-seed through pre-IPO, often packaged as the kind of SPVs this guide describes, so you get a front-row seat to the mechanics and access to the top 1% of deals. Join us at hustlefund.vc/squad.

.png)

.png)